Integrating ACH and credit card processing into your software or Internet ASP solution can make your payment processing cycle seamless. We have the documentation, code samples and technical assistance that will make this process easy. In addition the compliance burdens for credit card (PCI) and ACH processing are now on our shoulders rather than your […]

Search results for "user"

ChurchSquare Ecommerce Options

Use ChurchSquare and your customer billing headaches will be over.

Whether you need to bill a one-time payment or process monthly recurring charges you can rely on an economical, easy to use, built-in payment processing solution. You now have a seamless, automated and secure push button solution for debiting checking/savings accounts (ACH) and credit cards.

We provide a single gateway (secure payment data mover) that can process both electronic checks and credit cards. Payment histories are updated within ChurchSquare and can also be easily tracked via an online Virtual Terminal. Sensitive data is protected using PCI compliant tokenization so you are not burdened with compliance issues.

Pricing Information:

As a ChurchSquare user you qualify for special pricing considerations. You will have the ability to accept payments from credit cards and checking accounts [called an ACH]. You will have an ACH merchant account, credit card merchant account and a gateway account. The gateway is the secure pathway that payment data gets from ChurchSquare to payment processor.

$0 application fee.

Credit Cards: Interchange plus 30 basis points [.3%] and a per transaction fee = .22. An Interchange plan is the most economical for merchants because all card types start at MasterCard/Visa costs. Your fees are .3% above these costs.

ACH: Per transaction = .35 [flat 35 cents-no %]. Per return [example would be an NSF-non sufficient funds] = $2.50.

Gateway: .01 per transaction [1 penny].

Monthly: For three accounts plus reporting and 800# support your total outlay will be $20.00

Most gateway providers [Authorize.net] charge you .10 per gateway and $25/month JUST for the gateway account

You will apply for these accounts by filling out paperwork [tells us who/where you are] and along with voided check and two month’s bank statements fax/email/upload these documents to us. We typically will have you approved and able to process payments in 4-5 business days. If you are incorporated or an LLC we can obtain this info online. If you are a sole proprietor we may also need a dba [doing business as] certificate or equivalent.

To get started and apply online you may click here

To receive more information or receive documents via email send and email to info @ ach-payments.com. You may also call 888.729.2968.

Read full story • Comments are closed

Using an ACH Virtual Terminal (The 2023 Guide)

Table of Contents:

- What is an ACH Virtual Terminal

- Benefits of an ACH Virtual Terminal

- Why Recurring Payment Based Businesses NEED ACH Integration

- Case Study

- ACH Transaction Disputes

- Merchant Options

- Transactions

- Reporting

- Additional Resources

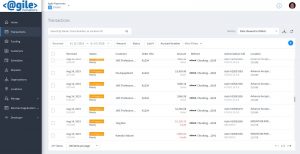

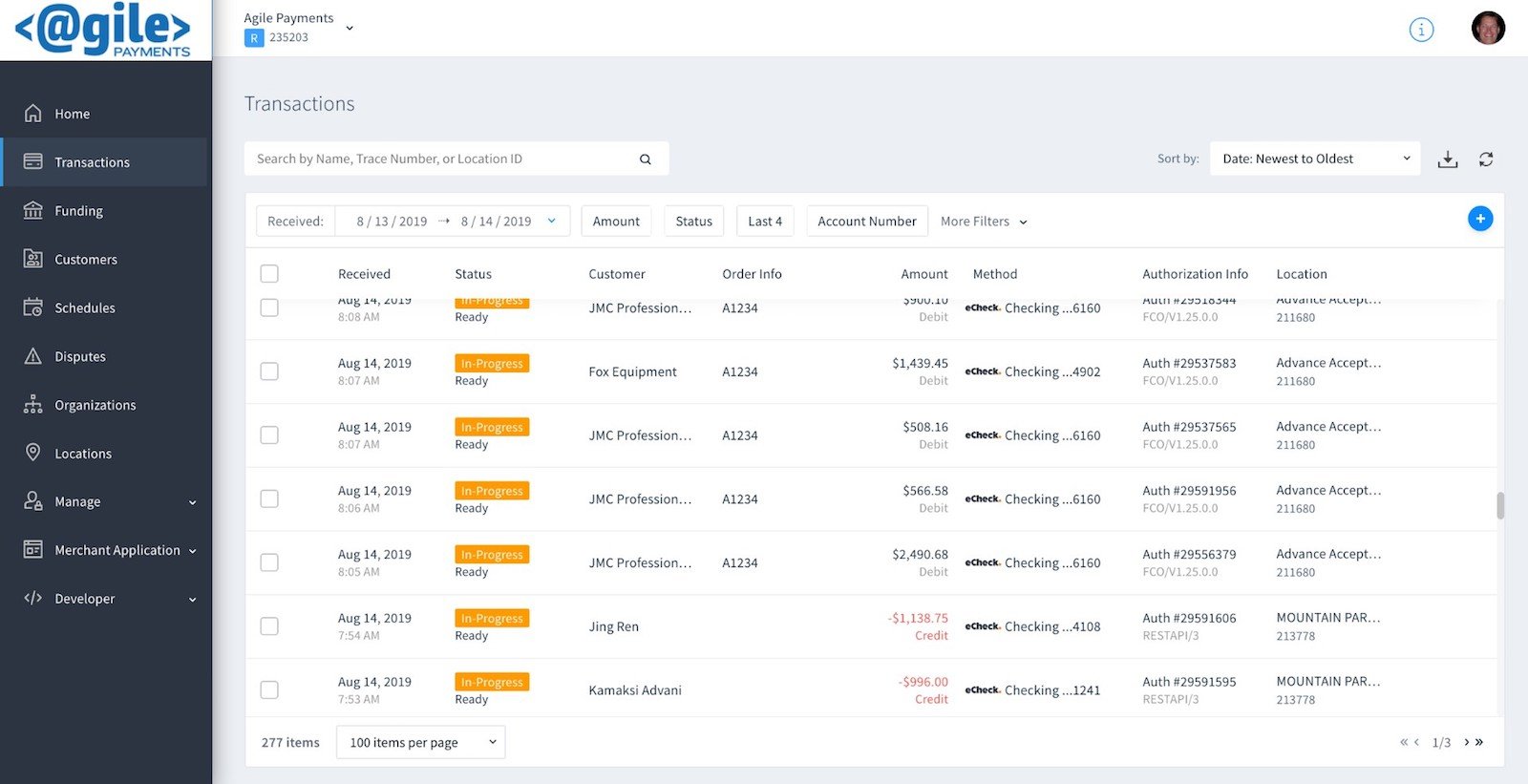

What is an ACH Virtual Terminal?

ACH Virtual Terminal

An ACH Virtual Terminal is a web-based hub that allows a person to securely accept single and/or recurring payments via ACH [echeck] or credit/debit card. A Virtual Terminal allows the management of Credit Card and ACH transactions, and provides originators with a secure, PA DSS certified, web browser software application for the transmission.

Transactions can be instant or scheduled, and scheduled transactions can be single future or recurring transactions. The ACH Virtual Terminal Solution can be utilized for transactions by organizations that have preexisting credit card merchant accounts. Most major back-end processors offer gateway communication, and payment data entry can be accomplished in numerous ways (e.g. manual data entry, file upload or machine read). Additional hardware is available for machine-read data entry for both ACH and credit card transactions.

An ACH Virtual Terminal offers the following benefits:

- Secure Payment Processing — Level 1 PCI compliant with credit card tokenization to ensure data integrity.

- Anti-Fraud Tools — Address verification, velocity controls, advanced checking account verification tools as well identity verification.

- Intuitive Interface — makes payment processing and reporting simple.

- Virtual Terminal Gateway — You can connect the Virtual Terminal to multiple back end credit card processors.

- ACH Website Payment Tools — Quickly create a secure hosted payment page with custom fields and the ability to take one-time or recurring payments.

- Comprehensive and Useful Reporting — Ability to export reporting into multiple formats. Create templates for your specific needs. The Transaction Funding Report is a differentiator. It’s a reporting tools that matches a funding deposit with the associated transactions that comprised that funding.

- Recurring Engine — Set up recurring payments with ability to use backup payment method. Revenue reporting based on future recurring transactions. Credit card expiration reports.

- Email Receipts — Offer customized messaging for your customers. These automated messages are an excellent opportunity for cross-selling/upselling customers.

- Payment Scheduling — Accept one-time payments for the present/ future date, and use multiple scheduling options for recurring payments.

- Individual Access Permissions for Multiple Users

- Hardware Support — Plug in a credit card or check reader via USB and swipe cards for auto-import into the Online ACH Virtual Terminal.

Utilizing an ACH Virtual Terminal Provider along with an integrated solution is a hybrid solution for leveraging Virtual Terminal Gateway Integration.

Businesses Utilizing a Recurring Payment Model NEED an ACH Transaction Integration for Multiple Reasons:

ACH Payment Integration allows payment options and benefits for the users of SaaS companies, including:

- ACH Processing fees are typically 80-90% less expensive than credit card fees.

- Credit card decline rates are on the rise. Average recurring credit card billing return rates are around 15%, while ACH payment processing return rates are typically less than 2%.

- Banking checking/savings accounts don’t have expiration dates, making them considerably less susceptible to being closed or re-generated due to data theft. This makes ACH integration an ideal choice for recurring payments based applications.

- ACH payments are widely accepted for payment facilitation by consumers/businesses.

Paper checks are burdensome. Checks are expensive to handle, susceptible to fraudulence, and simply don’t work for organizations/applications looking to accept payments from bank accounts. Beyond empowering a client’s software through API functionality, an ACH Payment Integration solution is a predictable, less expensive payment vehicle.

Case Study

An insurance company needed a payment collection tool their CS reps could use to securely accept ACH and credit card premium payments. Continue Reading →

Read full story • Comments are closed

Why ACH Integration?

ACH Payment Integration

SaaS developers and platforms can automate payment collection, disbursement and reconciliation through the use of an ACH API (Application Programming Interface). This ACH option allows debiting and crediting of checking and savings accounts via the ACH network.

ACH Payment Integration allows a SaaS companies’ users payment options and benefits. Businesses that utilize a recurring payment model NEED an ACH transaction integration for multiple reasons:

- Banking checking and savings accounts don’t have expiration dates and are not nearly as susceptible to being closed or re-generated due to data theft, making ACH integration of payments an ideal choice for recurring payments based applications.

- ACH payments are widely accepted for payment facilitation by both consumers and businesses.

- ACH Processing fees are typically 80-90% less expensive than credit card fees.

- Credit card decline rates are on the rise. Average recurring credit card billing return rates are around 15%, while ACH payment processing return rates are typically sub 2%.

What Should a Business Look For in an ACH Integration API?

- Can you leverage the ACH Processing Integration for your apps’ revenue stream?

- Is there an API that would allow your customers to apply from your site or app?

- Other payment utilities available?

- Does the platform meet PCI Security standards (though NACHA does not require ACH transactions to be PCI compliant)?

- Does the partner provide assistance in ACH payments processing adoption for you and your user clients?

- Does the ACH API offer additional utilities to make calls for anti-fraud and risk mitigation?

- For market bases that include Canada: does the partner provide a single API for both United States ACH and Canadian EFT?

- Is sensitive data tokenized?

- API availability: Does the partner offer RESTful or SOAP ACH transaction integration, or both?

- How long has your potential integration partner been serving the needs of app providers and what is their track record?

- Are there white label possibilities that might allow for a branded processing option, keeping the ACH processor behind the scene?

- Can risk acceptance models lower processing costs?

- Will your potential partner take the time to understand your business requirements and provide options that custom fit the payments needs to your needs and your clients?

- Advanced ACH reconciliation capabilities that enables matching payment bank deposits to platform reporting.

Why Else Should One Consider ACH Integration?

Paper checks are a burden, expensive to handle, and simply don’t work for organizations or applications wishing to accept payments from bank accounts. Paper checks are also susceptible to fraudulence than anything facilitated via an ACH Integration.

An ACH Payment Integration solution is a predictable, less expensive payment vehicle, and API functionality will empower your software and add value for your user base. This will inevitably lead to more satisfied clients.

Credit card transactions can be disputed and charged-back for a number of reasons. That’s not the case with ACH transactions. There are only three reasons that an ACH transaction can be disputed:

- The transaction was not authorized to be debited.

- The amount was incorrect

- The date that it was processed was incorrect.

ACH Integration and Payment Aggregation

An ACH Payment Aggregator or Facilitator can be thought of as being a Master Merchant who facilitates ACH transactions for sub-merchants within their payment ecosystem. Becoming an ACH aggregator or Payment Service Provider lends itself quite well to some businesses that fall into the software provider classification. Especially those who have recurring payments requirements via ACH integration.

The aggregation model was initially prohibited by credit card associations as well as the third party ACH processors. As PayPal grew rapidly it became clear that there was a lot of money to be made with aggregation. It became a model that the card associations had to embrace. While it’s still not widely provided by ACH processors, some have come to embrace the ACH aggregation model because of technological advances in KYC, advanced on-boarding processes and a better overall understanding of associated risks and mitigation processes to manage them.

The customer on-boarding process is a pivotal component for most organizations. To simply have an ACH Payment Integration option may not be enough. Many organizations prefer for the on-boarding process to be a “white label” process, meaning the third party ACH processor will remain in the background. The ACH integration must provide a way for the organization to pass their merchant’s data to the ACH processor’s underwriting department that requires it. This “passing” ideally occurs with everything in electronic format, including signatures.

The API must provide the ability for the application and underwriting process to be presented on their website, as though the ACH payments solution is coming from them. The underwriting data must be passed to the processor, the parties involved must be notified to where the application stands, and the API credentials must be passed to the applicant user once the merchant application has been approved and enrolled.

In some cases the credentials are passed to the merchant themselves. In the case a SaaS application the merchant user is required to enter API credentials themselves, and in other cases the API credentials are passed to the SaaS organization for entry on behalf of the merchant, depending on the ACH integration path that the SaaS organization chose.

Data hostaging is the inability for a merchant to receive non-tokenized card data in the event that they wish to switch merchant accounts, a situation that is becoming common in the credit card world. In some cases it’s simply prohibited by the processor, while in other cases a merchant must pay exorbitant fees in order to obtain the data. The process can be a long and arduous process, as processors try to delay the data transfer in order to maximize profits.

While ACH transactions do not fall under the same PCI scope as credit card transactions, most ACH processors who value sensitive data (and the potential theft of it) do tokenize ACH data in the same manner that credit card processors do.

A SaaS application can become the processor’s defacto sales organization for a payment processor. Many times this is predicated on whether the SaaS organization views the ACH integration as a payments partnership or wait to consider payment integration until near the end then choose a quick integration and be done with it (a mindset that is unfortunately all too common with developers). A payments partnership is a complex agreement, but the basics are that the SaaS organization and it’s using clients find an agreement among the rates, and that the processor can still find profit. Revenue share percentages can vary widely based on the reach and user base of the SaaS organization, but do your best at leveraging your application and it’s base in order to realize profit for yourself. After all, in a payments partnership, it’s your organization that is creating the leads for the processor.

Read full story • Comments are closed

Please read what some of our AutoPay users have to say about the program:

“Using the ACH Payments Studio Auto Pay has saved my business! I have literally gone from about 20 hours a week doing bookwork to about 4 hours a month! It has seriously freed me to work on my business which has almost tripled since we started using the ACH System!

Thanks Wayne!!!!

Christy Johnson-Dance Masters by Christy

“Hey Wayne: As we head into our busy Back-to-School season, I would just like to thank you for the excellent service you folks have provided us with. Before switching over to ACH Payments, we spent so much time and effort (read: ‘MONEY’!) chasing clients for receivables that we hardly had time for anything else. Since we switched our customers to Auto-Pay, we have found a lot more time to devote to business development. We experienced next-to-no objections about going this route, and this season you may see our activity almost double! Next year I expect my golf game to improve!! All the best, Corbit Larson, Centre Music House”

“Not only has ACH and Studio AutoPay saved me hundreds of hours this past year, but I have for the first time in 15 years I have a $0 balance for people owing me money AND I don’t feel frustration towards some of my usual late paying clients! “ACH is the best business decision I have ever made. I get ALL the money owed to me on the first of each month without any phone calls or statements sent out to students/clients. I have time to build my business, not wasting time collecting money!” Best wishes Wayne!!

Angie Ford, Terrace School of Music”

_______________________________________

HELPFUL FORMS:

Studio Auto Pay Application (Must be completed)

Credit Card Application (If you want to accept credit cards)

Sample Studio Auto App (shows how to fill the app out)

Credit Card Sample App (shows how to fill the app out)

Authorization for Payment (Parent form to be able to collect payments)

_______________________________________

JackRabbit Software: Our Preferred Studio management solution. The Mastermind edition of Jackrabbit combines the most powerful software in the studio business with the business building strategies of studio business coach Sam Beckford. The Mastermind edition incorporates advanced methods of tracking registration, retention and teacher performance with standard Jackrabbit software. Future enhancements to automate pre-registration and studio marketing functions are planned for the upcoming year. The underlying purpose of the Mastermind edition is not just to organize and automate the studio, but to provide functions that increase studio revenue and profit.

________________________________________

Supporting application documents should include:

* Articles of Incorporation or equivalent–the person signing the application should be authorized in the Articles.

* 2 months bank statements (not online banking copies)

* voided check

*copy of customer contract authorizing payments

* ONLY if processing more than $30k per month a tax return or audited financials are also needed.

If applying for credit cards as well please include the past 3 months credit card processing statements (if currently processing)

The application should be returned by mail ( or overnighted) to:

ACH Payments 15 Ingersol RD Saratoga Springs, NY 12866

Please contact us with any questions. Thank you.

FAQ’s

1) Can I use my bank to receive payments?

-Yes. You provide us a voided check on the bank account you would like funded.

2) How long is the approval process?

-3 to 4 days for ACH (checking/savings) and about 1 week for credit cards.

3) Is this safe for me and my students?

-Absolutely. All the transactions that you enter are done via a secure web site. Essentially that means you data is very safe and encrypted. Your students (and you) are protected by banking rules against unauthorized debits. The bank is legally obligated to replace funds taken without authorization (60 day window of time)

4) Do I need to have my student sign anything?

-Yes. If you are performing recurring debits you should have students sign an agreement stating they give you authorization to debit their account. You can obtain a sample form here (edit to your needs)

Authorization for Payment

5) Can you make changes to scheduled payments?

-Yes. each recurring payment can be easily edited.

6) Can I process one time and recurring payments?

-Yes. Both are easily accomplished.

7) How long have you been in business and can we be confident this product will meet our need now and in the future.

-YES. We have been in business for since 1998 and process millions of transactions for major companies and small businesses alike.

8) Any suggestions for implementing the program with our students?

-You should promote and push this option at every opportunity. IT SAVES TIME AND MONEY. You may seriously consider making participation mandatory.

9) How is support handled?

-You can call an 866.290.5400 for support 8am-7pm CST.

If you have additional questions please contact us.

Read full story • Comments are closed

Effective date: January 21, 2019

ACH Payments (“us”, “we”, or “our”) operates the https://www.ach-payments.com website (the “Service”).

This page informs you of our policies regarding the collection, use, and disclosure of personal data when you use our Service and the choices you have associated with that data. Our Privacy Policy for ACH Payments is created with the help of the Free Privacy Policy website.

We use your data to provide and improve the Service. By using the Service, you agree to the collection and use of information in accordance with this policy. Unless otherwise defined in this Privacy Policy, terms used in this Privacy Policy have the same meanings as in our Terms and Conditions, accessible from https://www.ach-payments.com

Information Collection And Use

We collect several different types of information for various purposes to provide and improve our Service to you.

Types of Data Collected

Personal Data

While using our Service, we may ask you to provide us with certain personally identifiable information that can be used to contact or identify you (“Personal Data”). Personally identifiable information may include, but is not limited to:

- Email address

- First name and last name

- Phone number

- Address, State, Province, ZIP/Postal code, City

- Cookies and Usage Data

Usage Data

We may also collect information how the Service is accessed and used (“Usage Data”). This Usage Data may include information such as your computer’s Internet Protocol address (e.g. IP address), browser type, browser version, the pages of our Service that you visit, the time and date of your visit, the time spent on those pages, unique device identifiers and other diagnostic data.

Tracking & Cookies Data

We use cookies and similar tracking technologies to track the activity on our Service and hold certain information.

Cookies are files with small amount of data which may include an anonymous unique identifier. Cookies are sent to your browser from a website and stored on your device. Tracking technologies also used are beacons, tags, and scripts to collect and track information and to improve and analyze our Service.

You can instruct your browser to refuse all cookies or to indicate when a cookie is being sent. However, if you do not accept cookies, you may not be able to use some portions of our Service.

Examples of Cookies we use:

- Session Cookies. We use Session Cookies to operate our Service.

- Preference Cookies. We use Preference Cookies to remember your preferences and various settings.

- Security Cookies. We use Security Cookies for security purposes.

Use of Data

ACH Payments uses the collected data for various purposes:

- To provide and maintain the Service

- To notify you about changes to our Service

- To allow you to participate in interactive features of our Service when you choose to do so

- To provide customer care and support

- To provide analysis or valuable information so that we can improve the Service

- To monitor the usage of the Service

- To detect, prevent and address technical issues

Transfer Of Data

Your information, including Personal Data, may be transferred to — and maintained on — computers located outside of your state, province, country or other governmental jurisdiction where the data protection laws may differ than those from your jurisdiction.

If you are located outside United States and choose to provide information to us, please note that we transfer the data, including Personal Data, to United States and process it there.

Your consent to this Privacy Policy followed by your submission of such information represents your agreement to that transfer.

ACH Payments will take all steps reasonably necessary to ensure that your data is treated securely and in accordance with this Privacy Policy and no transfer of your Personal Data will take place to an organization or a country unless there are adequate controls in place including the security of your data and other personal information.

Disclosure Of Data

Legal Requirements

ACH Payments may disclose your Personal Data in the good faith belief that such action is necessary to:

- To comply with a legal obligation

- To protect and defend the rights or property of ACH Payments

- To prevent or investigate possible wrongdoing in connection with the Service

- To protect the personal safety of users of the Service or the public

- To protect against legal liability

Security Of Data

The security of your data is important to us, but remember that no method of transmission over the Internet, or method of electronic storage is 100% secure. While we strive to use commercially acceptable means to protect your Personal Data, we cannot guarantee its absolute security.

Service Providers

We may employ third party companies and individuals to facilitate our Service (“Service Providers”), to provide the Service on our behalf, to perform Service-related services or to assist us in analyzing how our Service is used.

These third parties have access to your Personal Data only to perform these tasks on our behalf and are obligated not to disclose or use it for any other purpose.

Links To Other Sites

Our Service may contain links to other sites that are not operated by us. If you click on a third party link, you will be directed to that third party’s site. We strongly advise you to review the Privacy Policy of every site you visit.

We have no control over and assume no responsibility for the content, privacy policies or practices of any third party sites or services.

Children’s Privacy

Our Service does not address anyone under the age of 18 (“Children”).

We do not knowingly collect personally identifiable information from anyone under the age of 18. If you are a parent or guardian and you are aware that your Children has provided us with Personal Data, please contact us. If we become aware that we have collected Personal Data from children without verification of parental consent, we take steps to remove that information from our servers.

Changes To This Privacy Policy

We may update our Privacy Policy from time to time. We will notify you of any changes by posting the new Privacy Policy on this page.

We will let you know via email and/or a prominent notice on our Service, prior to the change becoming effective and update the “effective date” at the top of this Privacy Policy.

You are advised to review this Privacy Policy periodically for any changes. Changes to this Privacy Policy are effective when they are posted on this page.

Contact Us

If you have any questions about this Privacy Policy, please contact us:

- By email: [email protected]

- By phone number: 8887294968

- By mail: 15 Ingersoll Road Saratoga Springs, New York 12866, United States

Read full story • Comments are closed

Recent Video